this is the last in a multi-post series… part I is available here, part II is available here and part III is here.

When the EU announced the new €3 flat rate customs duty for low-value imports, many merchants immediately focused on the obvious question:

“How much more will this cost us?”

It’s the wrong question – if you’re an ambitious eCommerce merchant. The better question is:

“How much more will it cost our competitors?”

Over the last few posts, we explored the uncertainty surrounding the new €3 duty. First, we examined the unanswered question at the centre of the reform: what exactly is the €3 charge applied against? That has now been answered with relatively little doubt (and, thankfully, our original interpretation was correct – phew…!)

Then we looked at the consequences of getting that answer wrong. Not from a compliance perspective (because nobody really worries about compliance, right..?), but from a commercial one. Incorrect assumptions can distort landed costs, inflate customer charges and create pricing disadvantages that are completely avoidable within the rules.

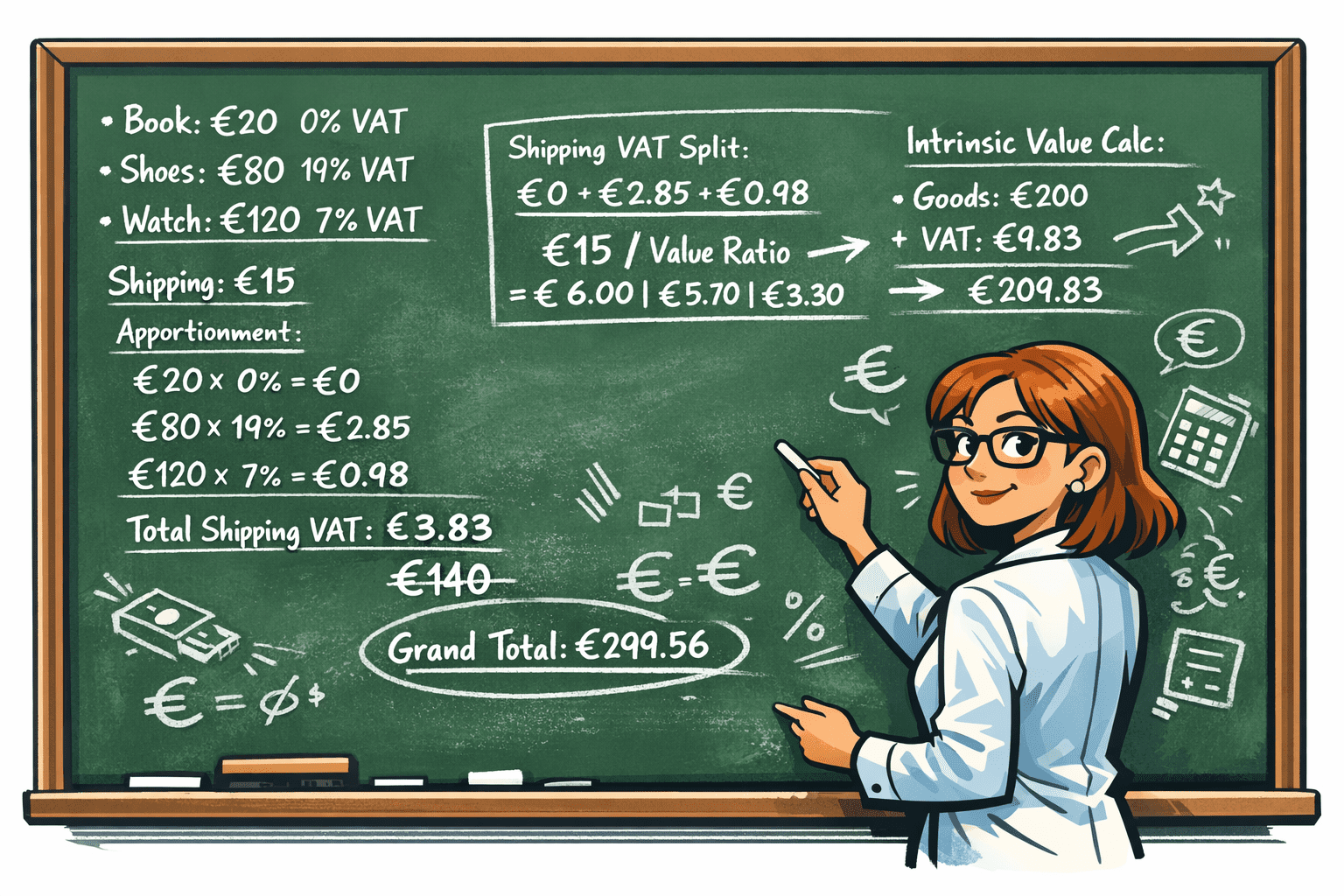

Finally, we demonstrated that the same basket of goods can legitimately produce different customs outcomes depending on how it is structured and declared.

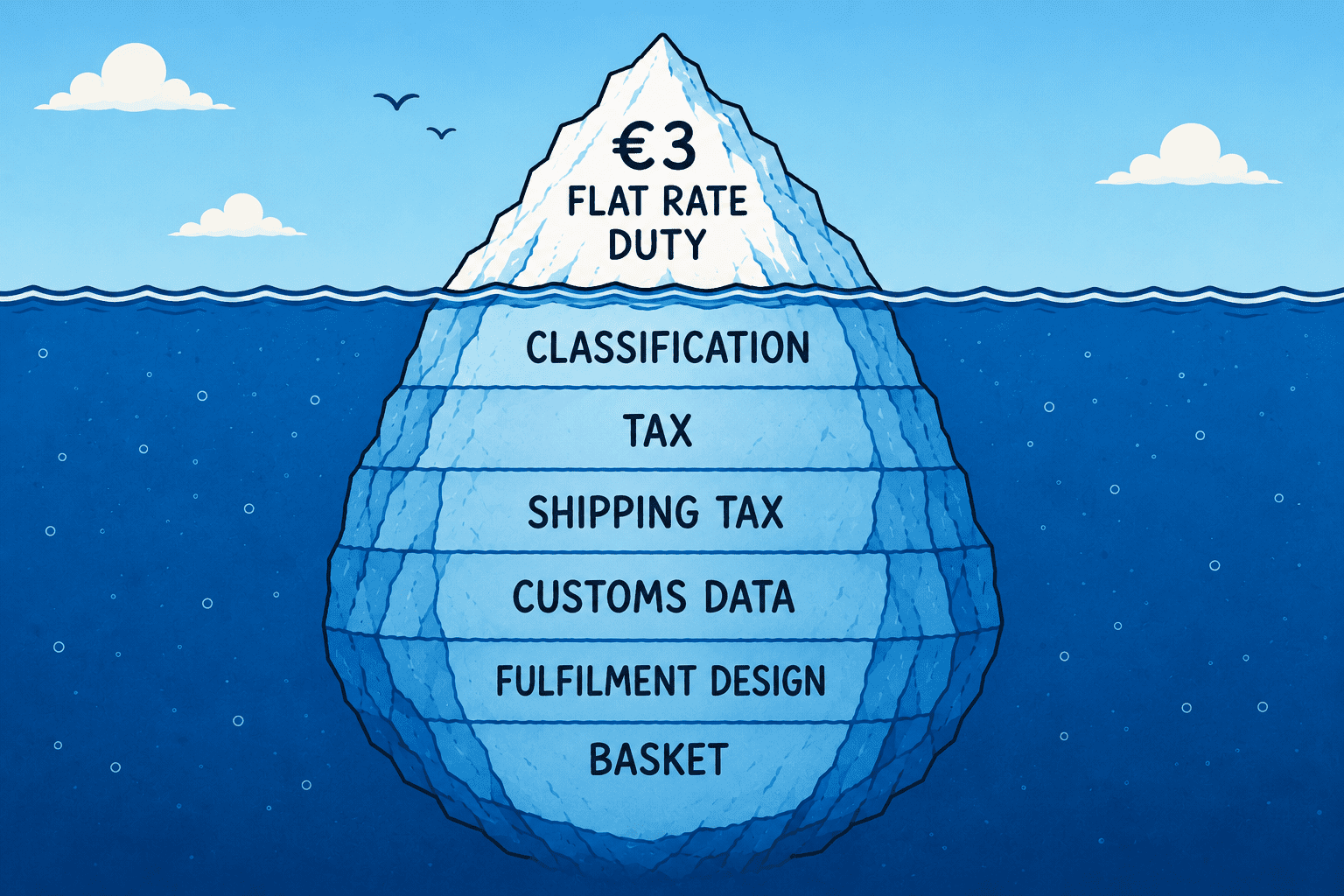

That last point matters more than many merchants realise, because the new duty is not really a product problem – it is a data problem. When the Product data is incorrect, everything downstream is also incorrect. That includes Taxes, Duties and Customs Declarations.

Historically, many cross-border merchants could afford to treat customs classification as an administrative afterthought. A product description was entered, a shipping label was generated and the parcel moved.

The economics of that approach are changing as a result of these new regulations. And, like all regulation-driven innovation, merchants can choose to see this as an inconvenient and frustrating imposition or an opportunity to leverage the rules while competitors are struggling to come to terms with them (this is the philosophy we built ePAL on, as discussed in an interview with Kumar Dattatreyan).

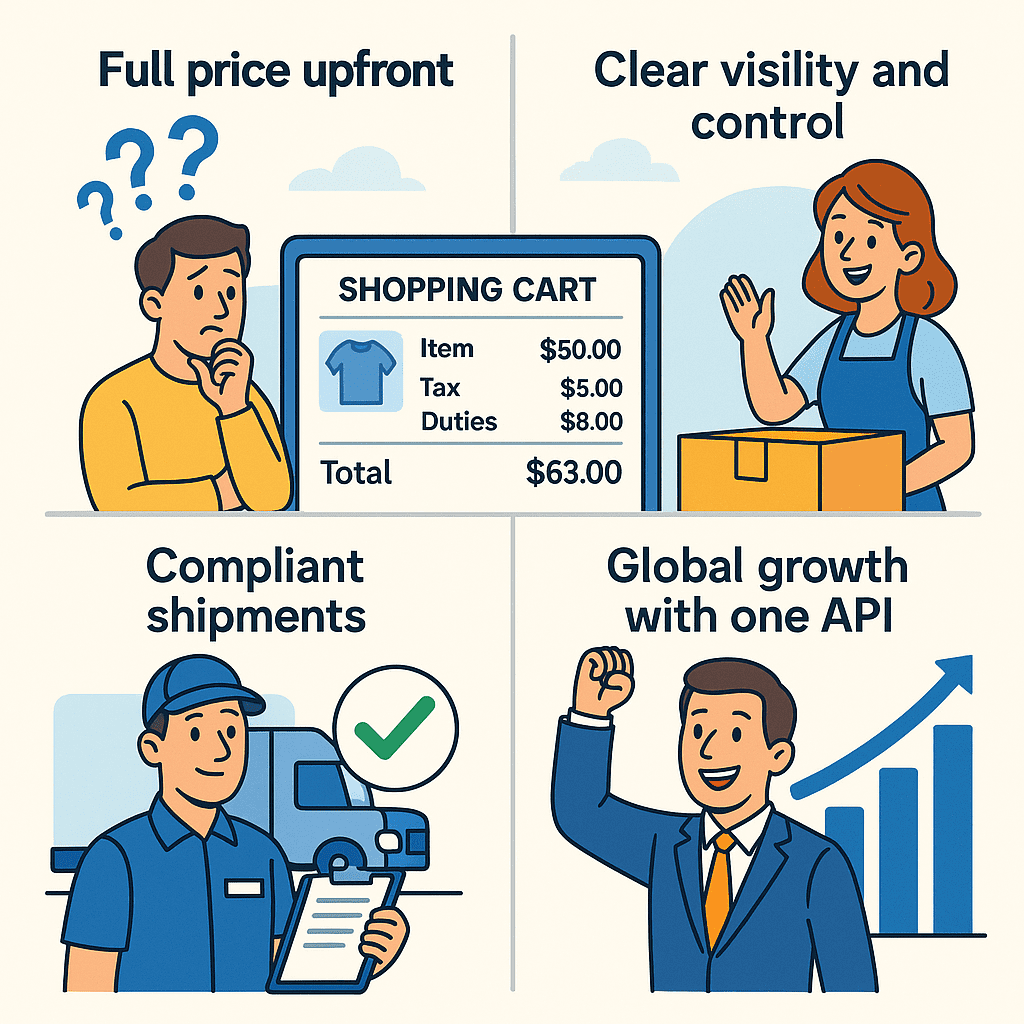

From July 2026, customs classification, basket composition, declaration structure and fulfilment decisions will directly influence landed cost outcomes. Two merchants selling similar products at similar prices may end up producing very different customer experiences.

One customer sees a smooth checkout with predictable costs. Another sees unexpected charges, abandoned baskets or higher total prices. The products may be identical. The difference is intelligent and intentional operational design. This is where many businesses will discover that the challenge is larger than the €3 charge itself.

Most merchants do not have customs specialists reviewing every order. They do not have teams manually evaluating tariff classifications. They do not have people calculating different fulfilment scenarios in real time. And they certainly do not have staff checking whether one declaration approach produces a better outcome than another while remaining compliant.

At scale, that is impossible. The only practical answer is automation. Not automation that simply calculates tax (tax is irrelevant in this context and, in fact, for merchants expecting their Tax calculation plugins or service providers to ‘deal with this’… don’t hold your breath).

And it is not enough just automate identification of duty rates any more. The real opportunity presented to forward-thinking merchants by this new regulation is automation that understands and leverages the relationship between products, classifications, basket composition, fulfilment models and destination-country requirements.

In other words, automation that treats customs and tax as part of the checkout journey rather than as an afterthought that happens after payment. That is the opportunity ePAL was built for – the core of ePAL is a complex orchestration engine and this new regulation is just another orchestration for us… and so it should be for you.

While much of the market is still discussing the €3 duty as a new cost, we see it as an orchestration & optimisation challenge.

Merchants need visibility into the full landed cost outcome before an order is placed. They need systems capable of understanding how different products interact within a basket. They need compliant calculation of tax, duties, shipping taxes and destination-country requirements. And increasingly, they need technology capable of identifying opportunities that would be practically invisible to humans operating manually.

The reality is that the July 2026 reforms will not affect every merchant equally.

- Some businesses will simply absorb higher costs.

- Some will pass those costs to customers.

- Some will discover that their existing processes are no longer competitive.

Others will adapt. They will build smarter checkout experiences, make better fulfilment decisions, understand their customs data more deeply. And they will turn what looks like a regulatory burden into a commercial advantage.

The €3 duty was introduced as a simplification measure.

Ironically, it may end up rewarding the merchants who understand complexity best.

That is exactly the problem ePAL was designed to solve.