In eCommerce, there is a particular phrase that sounds reassuring while doing very little real work: “The €150 IOSS threshold is simple”. It is usually said by someone who has not had a shipment stopped, a customer refuse delivery or a courier ask for money that nobody expected to pay.

The €150 threshold is viewed as a clean dividing line. Below it, life is easy. Above it, things get complicated. Unfortunately, this mental model is wrong in just enough ways to cause problems at scale.

Let’s dispel this ‘myth’ with an accurate and (hopefully) useful explanation – not theory or marketing. Just how the threshold actually behaves in the real world of cross-border eCommerce.

What the €150 threshold is supposed to do

At a policy level, the €150 threshold exists to reduce friction on low-value imports into the EU. If a consignment qualifies for IOSS:

- VAT is collected at checkout

- Customs duties do not apply

- The parcel should clear customs without the buyer being asked for additional payment

This is the intent: reduce friction, improve predictability & keep low-value purchases moving. None of that is controversial. The problems start when the threshold is treated as a price tag, rather than what it really is: a valuation test performed using explicit rules set by Customs authorities

The first misunderstanding: €150 is not the checkout price

Merchants often assume the threshold is evaluated against:

- The price shown to the customer, or

- The amount charged to the card, or

- The order total in the store currency

None of these are correct.

The IOSS threshold is assessed against something called intrinsic value, calculated:

- In euro

- Using customs rules

- Using customs exchange rates

- After removing certain taxes

- Before adding certain other charges

This already tells you something important.

If your store does not explicitly calculate intrinsic value using the same rules as customs, then the €150 threshold is being guessed, not calculated.

What “intrinsic value” actually means in practice

Intrinsic value is the customs valuation of the goods themselves, excluding some things and including others.

In practical terms, that means:

- The value of the goods only

- Excluding transport and insurance, but only if they are shown & priced separately

- Excluding any Tax that might already be included in the ‘source’ country

- Calculated in euro

- Using the official customs exchange rate, not your checkout FX

This is where many otherwise competent systems fall over. Merchants price for customers. Customs values for regulators. These two worlds are not aligned.

Currency: the silent breaker of assumptions

Most eCommerce systems use:

- Live FX rates

- PSP or card network conversions

- Daily or even intraday pricing logic

Customs does not.

EU customs authorities publish monthly exchange rates that remain fixed for the entire period. These rates are authoritative for customs valuation and deliberately insulated from market volatility. The consequence is uncomfortable but unavoidable:

- A basket that appears to be €149.50 at checkout may be €150.20 for customs purposes.

So what…? Well, it means that your basket is no longer eligible for streamlined IOSS treatment – but you will probably never know that because your order records show it as €149.50.

Nothing about the product changed. Nothing about the customer changed. Only the valuation framework changed: FX rates at checkout are different than FX rates published as much as a month ago and used by customs.

If the system evaluating IOSS eligibility does not use the official customs FX rate, the result is not “approximately correct”. It is simply wrong.

Tax removal before tax addition (yes, both happen)

Another common error is assuming the threshold test is performed on a price that already includes source-country taxes. It isn’t.

Where product prices include tax from the origin country, that tax must be removed before the intrinsic value is calculated. Only then is destination-country VAT applied for the purposes of calculating DDP (aka Fully Landed Cost). Note: Destination-country VAT is calculated separately for DDP (Fully Landed Cost) purposes and is not part of the intrinsic value test.

This matters because:

- VAT rates differ by product

- VAT rates differ by country

- Mixed baskets compound the effect

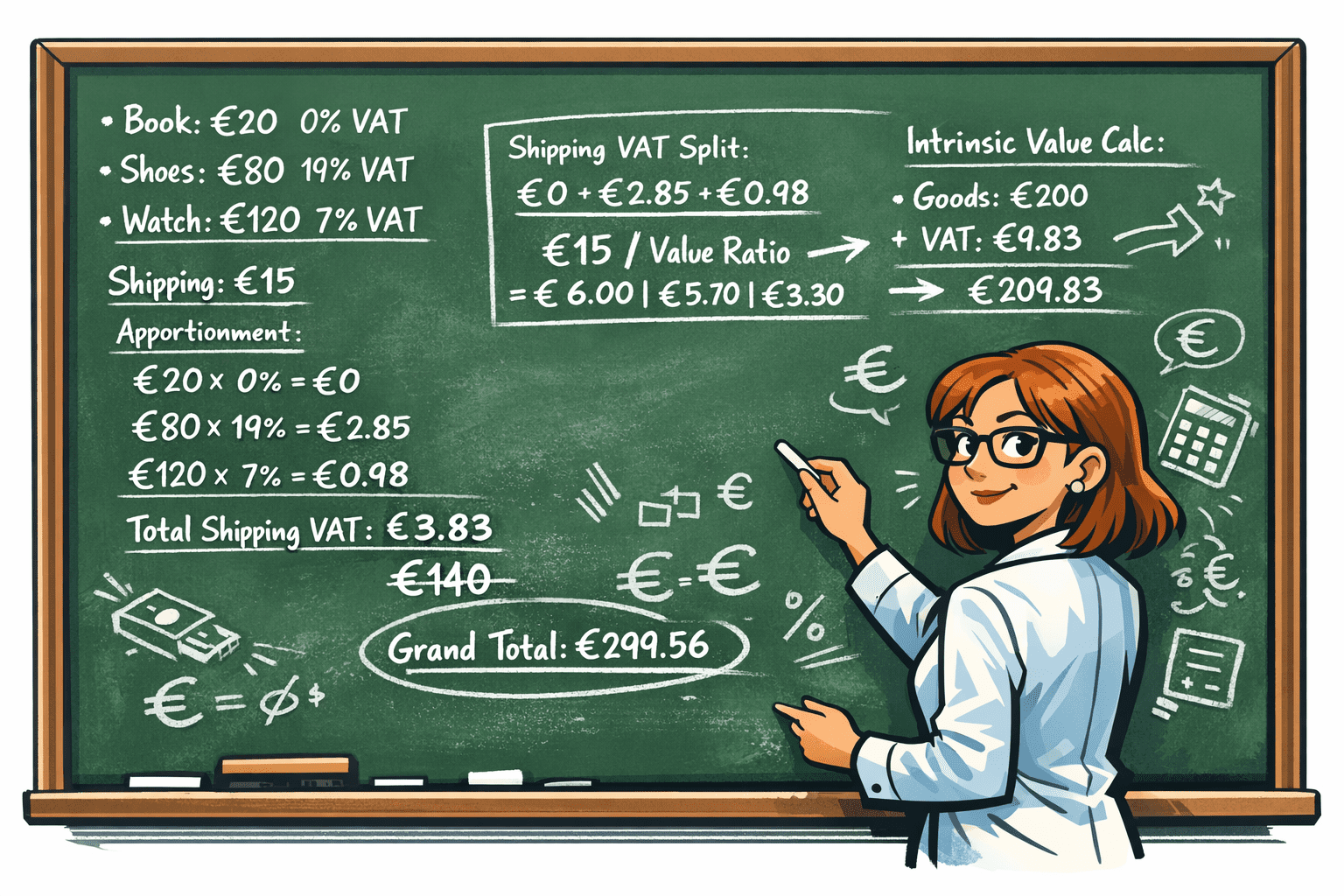

Shipping: excluded, except when it isn’t

The formal definition of intrinsic value excludes shipping when it is separately stated.

That sounds simple until you encounter:

- Free shipping models

- Bundled pricing

- Promotions where shipping is partially absorbed

- Platforms that do not break shipping out cleanly

- Mixed baskets where some products have shipping included in the price and others don’t

At that point, the question becomes not “is shipping excluded?” but “can shipping be cleanly excluded?”

If it cannot, customs authorities may treat part of that value as belonging to the goods themselves.

This is one of those areas where “probably OK” turns into “held at the border”.

The threshold is per consignment, not per product

Another persistent misconception is that multiple low-value items remain low-value when shipped together. They don’t. The €150 test applies to the entire consignment, not individual SKUs.

Two €80 items shipped together are not two IOSS-eligible products. They are one non-IOSS-eligible consignment.

This sounds obvious when stated plainly. It is surprisingly easy to miss when orders are built dynamically, split across fulfilment locations, or merged downstream by carriers.

Why “close enough” fails disproportionately

Many merchants adopt a pragmatic approach:

- Assume eligibility below a comfortable buffer

- Pad pricing slightly

- Rely on carriers to resolve edge cases

This works until volume increases.

The failure mode of IOSS misclassification is asymmetric:

- Ten correct orders go unnoticed

- One incorrect order causes a visible delivery problem

- The customer only remembers the failure

This is why merchants often believe they “mostly get it right” until the day they don’t and the cost lands all at once. In reality, merchants might not even know it’s a problem – the customer simply doesn’t buy again

The real cost of getting the threshold wrong

When an order is incorrectly treated as IOSS-eligible:

- Customs duties may suddenly apply

- VAT may be recalculated at import

- Carriers add handling fees

- Customers are asked to pay at the door

- Deliveries are refused

- Returns become complex or impossible

- VAT reporting no longer matches reality

None of this shows up in conversion metrics. It shows up in support tickets, negative reviews, and quietly eroded trust.

Why merchants should not try to “manage” the threshold

The €150 threshold is not a pricing decision.

It is not a marketing lever.

It is not a UX choice.

It is a regulatory classification that must be evaluated using rules most checkout systems were never designed to handle.

Trying to manually align:

- Live checkout FX

- Fixed customs FX

- Destination VAT rates

- Mixed baskets

- Shipping allocation

- Consignment logic

…is not a matter of effort. It is a matter of architecture.

This is why spreadsheets, plugins and carrier calculators inevitably diverge.

The only workable model: separation with mediation

The practical solution is not to force checkout pricing to behave like customs valuation, or vice versa. Each serves a different purpose. The workable model is to allow both to operate as intended and introduce a system that can:

- Perform the correct intrinsic value test internally

- Using the correct customs valuation and FX logic

- In real time

- Before the customer ever sees a final price

At that point, the outcome is binary and defensible:

- Either the consignment qualifies for IOSS

- Or it does not and must follow a different path

There is no ambiguity and no post-delivery correction.

What “explained properly” really means

The €150 IOSS threshold is not complicated because regulators enjoy complexity.

It is complicated because it sits at the intersection of:

- Tax law

- Customs valuation

- Currency policy

- eCommerce pricing behaviour

Treat it as a number and it will betray you. Treat it as a process and it becomes predictable. That predictability is the real prize. When merchants can trust that every order has been classified correctly before it ships, the downstream chain stabilises. Fewer delays. Fewer refusals. Fewer arguments at the door.

The threshold itself does not become simpler – but the business impact does. That is the difference between knowing about the €150 limit and actually understanding it.