…this is the first post in a multi-post series… part II is available here, part III is here and part IV is here.

Three pairs of trainers. Same price. Same category.

Three different answers.

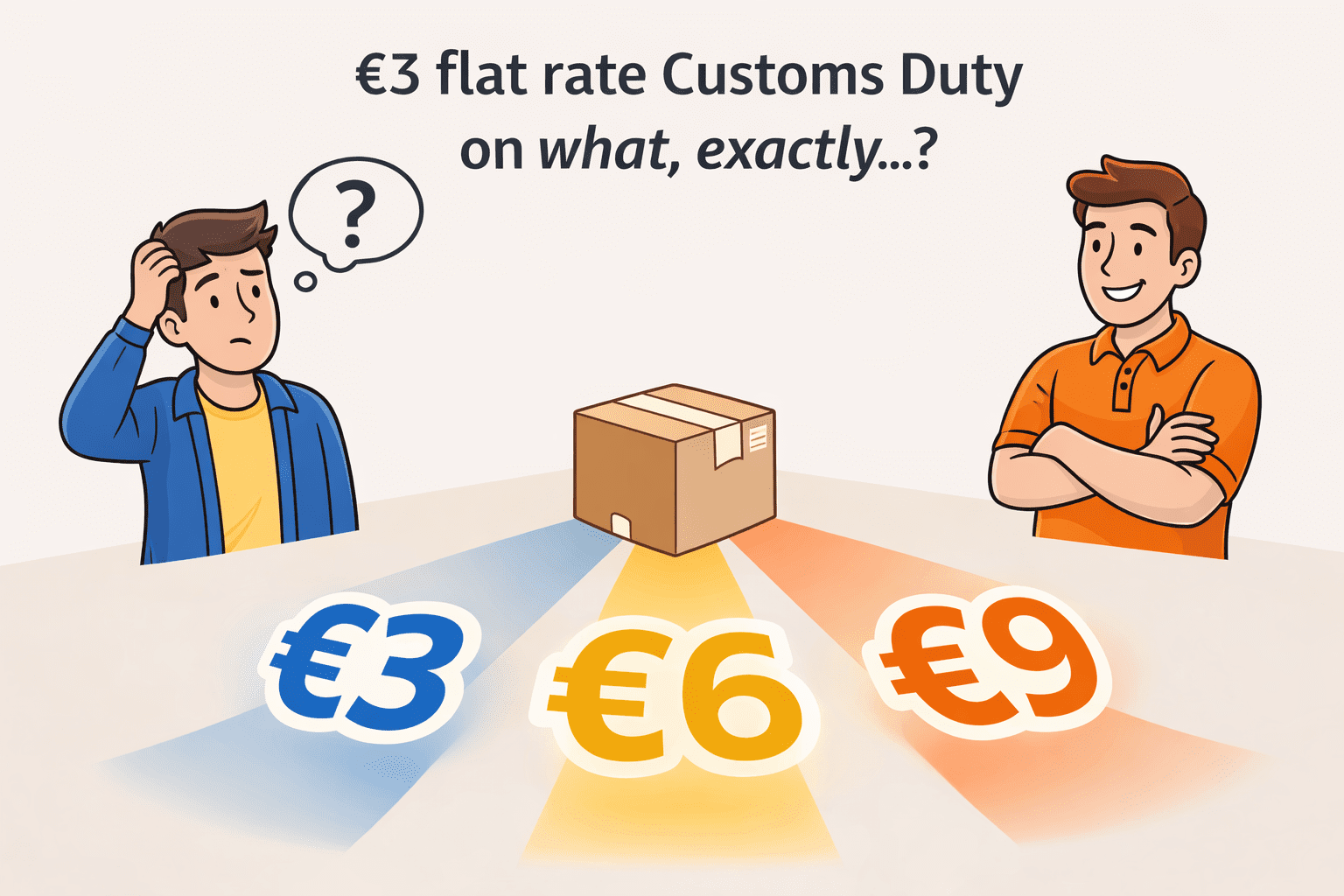

From 1 July 2026, the EU will introduce a flat €3 duty on low-value imports under €150. It is presented as a simplification. A pragmatic step. A way to deal with billions of small parcels without turning every shipment into a full customs exercise.

On the surface, it feels refreshingly straightforward. A small, predictable charge. Easy to explain. Easy to implement. Until you ask one simple question: €3 per what, exactly?

A simple basket that is not simple

Let’s ground this in something tangible. A merchant sells three pairs of trainers:

- 1 × Leather trainers – €50

- 1 × Textile trainers – €50

- 1 × Rubber or plastic trainers – €50

Total product value: €150

To any reasonable person, this is a simple basket. Three pairs of trainers. Same category. Same use. Same checkout experience. From a customs perspective, however, they are not identical.

All three can sit within the same HS6 family. At that level, they can reasonably be treated as one category. But at more granular levels, they diverge:

- Upper material

- Construction

- Composition

At CN8 or TARIC level, these differences can place them into distinct tariff sub-headings.

Now apply the €3 rule.

- If treated as one category → €3

- If treated as three categories → €9

Same basket. Same customer. Same checkout. Different outcome.

The missing definition

The official language refers to:

- “item category”

- “tariff sub-heading”

These are not merchant terms. They are customs concepts. And critically, they are not defined at a single level of granularity. So the ambiguity is immediate:

- Is the €3 applied per HS6 code?

- Or per CN8 classification?

- Or per TARIC sub-heading?

- Or per customs declaration line?

The regulation defines the price. It does not clearly define the unit.

Why the unit matters

If this were a percentage duty, classification nuance would matter, but it would not fundamentally change the structure of pricing. This is different. The total duty is:

€3 × number of “types”

So the number of times you apply €3 becomes the dominant variable.

Back to our trainers:

- Grouped at HS6 → 1 type → €3

- Split at CN or TARIC → 3 types → €9

That is a 3× difference, driven entirely by how you classify products that, to a customer, look interchangeable. This is not a rounding issue. This is pricing driven by taxonomy.

When accuracy becomes a disadvantage

Now consider two merchants selling exactly the same three pairs of trainers.

Merchant A:

- Classifies at HS6 level only

- Groups all trainers together

→ Applies €3 total

Merchant B:

- Has a more advanced system

- Classifies to CN or TARIC level

- Distinguishes material and construction

→ Applies €9 total

Same goods. Same value. Same destination. Different duty. The only difference is classification capability. This creates a structural problem:

- More accurate classification → higher duty

- Less granular classification → lower duty

Better compliance leads to a worse commercial outcome. That is not a theoretical concern. It is an incentive.

The predictable response

Faced with this, what will rational merchants do?

They will simplify.

Not because they want to be non-compliant, but because the system rewards it. Our trainers example makes this obvious. At HS6 level, there is a defensible grouping. The customer sees “trainers”, not “tariff sub-headings”. And nobody (official) has said it will be wrong.

So the merchant asks: Why would I split this into three categories and charge my customer €9 instead of €3? This is not abuse in the traditional sense. It is optimisation within ambiguity. And if one merchant does it, all merchants must follow.

The enforcement dilemma

This leaves customs authorities with an uncomfortable choice.

Option 1: Enforce granular classification

- Require CN8 or TARIC-level distinction

- Result: accurate classification but higher duty burden for compliant merchants

Option 2: Allow grouping

- Accept HS6-level aggregation

- Result: lower, more consistent duty but loss of granularity and control

Neither outcome is clean. Now scale that across millions of consignments. And across 27 Member States.

The fragmentation risk

The EU is a customs union in principle. In practice, implementation often varies at the edges. This rule sits squarely in one of those edges. Different Member States could:

- Interpret “tariff sub-heading” differently

- Apply different expectations on grouping

- Enforce classification at different levels

Back to our trainers:

- Enter via Country A → treated as 1 category → €3

- Enter via Country B → treated as 3 categories → €9

Same shipment. Different entry point. Different duty. At that point, this is no longer just a classification issue. It becomes a routing and market distortion issue.

The simplification trap

Merchants and platforms will try to “solve” this quickly. The most common shortcuts will look sensible. And they will be wrong.

- €3 per shipment

Our trainers → €3

Simple and predictable, but incorrect if multiple categories exist.

- €3 per line item

Three line items → €9

Feels logical from a checkout perspective, but line items are commercial constructs, not customs classifications.

- €3 per SKU

Three SKUs → €9

Operationally convenient, but SKUs reflect catalog design, not tariff logic.

- €3 per unit

Three units → €9

Clearly incorrect, but it will happen.

This is not a small edge case

It would be easy to dismiss this as a technical nuance. It is not. Return to the example. Three pairs of trainers. €150 basket.

- €3 duty → 2% uplift

- €9 duty → 6% uplift

That difference feeds directly into:

- Checkout pricing

- Conversion rates

- Customer perception

And critically, it is not driven by value or risk, but by classification structure.

Where this leaves us

We have a rule that is simple in isolation, but ambiguous in application. We have:

- No clearly defined classification level

- No published grouping standard

- No guidance on ensuring equitable treatment

And we have a system that:

- Incentivises simplification

- Risks fragmentation

- Produces different outcomes for identical goods

All from a €3 charge.

The unanswered question

So we come back to the only question that matters. At what level must goods be classified for the purposes of applying the €3 duty? Until that is answered:

- Every implementation is making an assumption

- Every merchant is making a trade-off

- Every checkout price is, to some extent, provisional

Closing thought

Three pairs of trainers. Same basket. Same customer. Same value. The only variable is how you choose to describe them. And yet, that description determines whether the duty is €3 or €9.

Sometimes the cost is not in the €3 flat rate. It is in how many times you have to apply it. And that’s before you factor in the non-price implications of the choice:

- How does it impact on VAT / Import Tax calculation?

- How does it impact on IOSS eligibility?

- How does it impact on what you include on the Customs Declarations?

…more next time…

If you want to find out more about how ePAL Global can help you not only prepare for the new cross-border reality but also to get ahead of it and optimise your product catalogue as well as your fulfilment and shipping flow, feel free to visit www.ePALGlobal.eu/landing if you are a WooCommerce user or www.ePALGlobal.com if you use a different platform or custom-developed web store.

Ron, nice explanation as usual. I know you read closely the regs, I can’t believe this is not clarified with only month before it kicks in. Crazy. David

Timing is everything, really glad to see a company on TOP of this prior to the release of these new REGS!

[…] the previous post about the new €3 “flat rate” EU Customs Duty for low value cross-border imports , we […]

[…] the first post in this series [“The €3 flat rate duty and the important unanswered question (pt.1)”], we asked a simple […]

[…] is the last in a multi-post series… part I is available here, part II is available here and part III is […]