In part one of this series we asked about the new €3 “flat rate” EU Customs Duty for low value cross-border imports , we asked a simple question: what is the €3 flat rate duty actually calculated against? It sounds trivial on the surface, but as we explored, the answer is far from clear.

The previous post focused on the ambiguity at the heart of the rule. This one is about the consequences of that ambiguity, because once you move past the question of “€3 per what?”, a more important realisation appears. The €3 itself is only part of the problem. What happens after only makes it worse.

Since then, we engaged with Regulators to ask them what ‘categorisation’ they plan to use and the general response was: “We don’t know yet” (yes, that’s the Regulators). The clearest response we received was:

…the €3 will be charged “per position in the import customs declaration”.

Hmmm… not the most helpful when it comes to clarity – but at least it’s a starting point!

Same basket, different outcomes

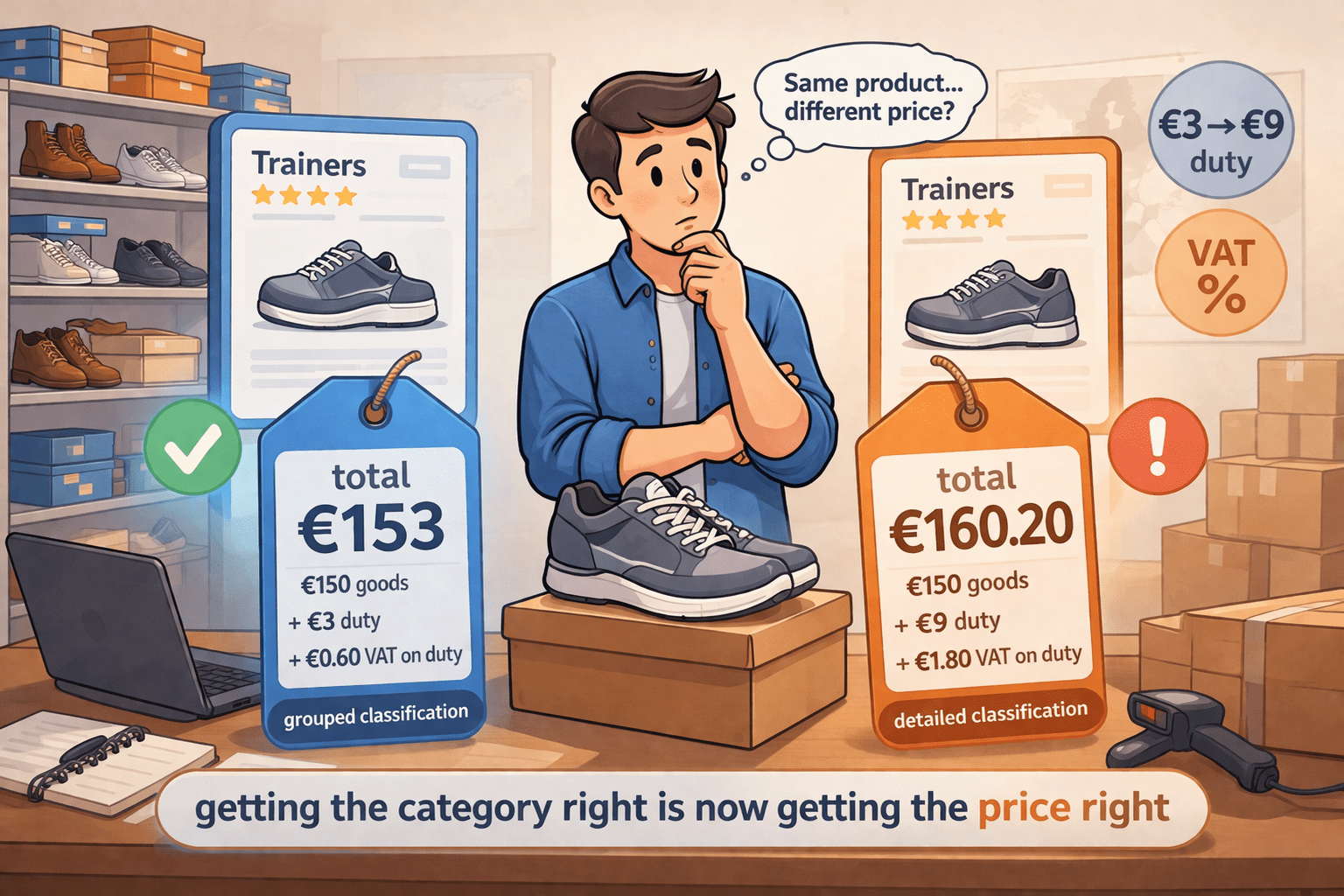

Let’s go back to the same example we used for illustration purposes in the previous post. A merchant sells three pairs of trainers made from different materials: leather, textile and plastic, each priced at €50. From a customer perspective, this is a simple, coherent basket with a total value of €150. There is nothing unusual or complex about it.

From a customs perspective, however, things diverge quickly. Depending on how those products are classified and grouped, the €3 rule produces two very different outcomes. If treated as a single category, the duty is €3. If split into three distinct categories, the duty becomes €9.

It is the same basket, for the same customer, with the same intrinsic value. The only variable is how the products are described within the system. That was the problem outlined in Part 1. But the impact becomes even more pronounced (i.e. more expensive for your customers & more detrimental to your business) once you follow that difference through the rest of the calculation.

Duty does not stay contained

It would be convenient if duty were the end of the story – a small adjustment applied at the edge of the transaction. In reality, duty is an input into several other calculations and those calculations determine the final price that the customer actually sees (whether that is in the checkout or when the delivery arrives at the door accompanied by a demand for extra payment).

Once duty changes, everything built on top of it changes as well. VAT is recalculated, total landed cost shifts and the checkout price moves accordingly. What initially looks like a €3 versus €9 issue becomes more significant. Getting duty wrong does not stay contained. It spreads.

Wrong duty = wrong tax on duty

This is not a new concept. We have seen the same dynamic before in a different context, as discussed here:

https://imaginef1.shop/2025/11/27/not-all-products-are-created-equal/

In many import scenarios, VAT or Import Tax is calculated not only on the value of the goods and shipping but also on the duty itself. This creates a compounding effect. If the duty is incorrect, the VAT calculated on that duty will also be incorrect. If you unnecessarily calculate Customs Duty (flat rate or otherwise) too high, then you also add too much VAT – and you will most likely never know.

Applying this to the earlier example makes the point a bit more concrete. If the duty is €3 and VAT is applied at 20%, the VAT on duty is €0.60. If the duty is €9, the VAT on duty becomes €1.80. The difference in VAT alone is €1.20, entirely driven by how the €3 rule is interpreted. That’s on top of the potential €6 overcharging of “flat rate” duty.

When combined with the €6 difference in duty, the total variance at checkout becomes €7.20. That is not a rounding error. It is a visible price difference for the same goods, created purely by classification decisions. For a basket that is nominally €150, the “fully landed cost” will either be €153.60 or €160.80. That is a significant difference.

Where this becomes real

At this point, the discussion moves out of the world of tax logic and into the reality of commerce. Two merchants selling identical products can now present different final prices to the same customer, based solely on how they apply the rule.

The customer does not see tariff sub-headings or classification logic. They see one price that is lower and one that is higher – and they make a ‘where to buy‘ decision based on that. It does not require a large difference to influence behaviour. It simply needs to exist.

That difference can affect which product appears first when the customer clicks ‘order by lowest price‘, which option feels more attractive and ultimately which merchant secures the sale. What began as a classification nuance becomes a direct input into revenue.

There is no safe error

It might be tempting to assume that there is a safer direction to lean in, perhaps by being conservative and charging more to avoid risk. In practice, both directions introduce problems.

Overcharging, by applying too many €3 duties, results in a higher checkout price. This reduces competitiveness and directly impacts conversion rates. Customers are unlikely to choose the more expensive option when alternatives exist.

Undercharging creates a different set of issues. If too few €3 duties are applied, the shortfall may be corrected later in the process, often at the point of delivery. This leads to additional charges, customer frustration and – in many cases – refused deliveries and returns.

There is no safe error. There are only different consequences, and both are potentially commercially damaging.

What the system encourages

Faced with this situation, merchants will behave rationally. They will optimise for lower checkout prices and higher conversion rates, because those are the metrics that drive their business.

In practice, this means simplifying classification where possible and grouping products at higher levels. This is not necessarily an attempt to avoid compliance. It is a response to the incentives created by the system itself.

The unintended outcome is difficult to ignore. The more precisely goods are classified, the more likely it is that additional €3 charges will be applied, increasing the final price. The system, as it stands, quietly rewards less granular classification.

That is not a stable or desirable equilibrium and it is difficult to believe this is the behaviour Regulators wanted to encourage.

What this means in practice

This is not a problem that can be solved with simple shortcuts. Approaches such as applying €3 per shipment, per SKU or per unit may appear convenient but they are not aligned with how customs defines goods. Each of these shortcuts introduces inaccuracies that surface either in pricing or in fulfilment.

Instead, merchants are left making decisions in an environment where the rules are not fully defined (yet, at least). They must determine how to classify their products, how to group them, and how to apply the €3 rule in a way that is both defensible and commercially viable. Consider that the poor merchant who sells three types of trainers might actually sell a dozen different forms of footwear with a dozen different classifications.

This is not a trivial exercise. It requires judgement, consistency and a willingness to revisit decisions as guidance evolves (or it requires ePAL..!)

What merchants should do now

Until clearer guidance emerges, the most practical approach is to focus on consistency and awareness rather than perfection. Merchants should be explicit about the level of classification they are using and apply their grouping logic consistently across transactions.

Perhaps most importantly, this should be treated as a pricing problem as much as a tax problem. The impact is ultimately visible at the point of purchase and that is where it matters most.

For merchants who have not already classified their products using Customs-specific classification, this must be the first port of call – even long before the duty classification rules are defined & published. No matter what they are, the rules will be based on standard Customs classification that already exists (that’s the one thing we learned from Regulators!).

Luckily, merchants can classify products to HS6 level using ePAL Global with no cost & no commitment.

Bringing it back to the core idea

In Part 1, the issue was uncertainty. In Part 2, the issue is consequence. The €3 rule was introduced as a simplification but in practice it has shifted complexity into classification, grouping, and interpretation. That complexity does not remain hidden in systems or documentation. It surfaces in the final price presented to the customer, where even small differences can influence behaviour and outcomes.

Getting the category right is no longer just about compliance. It is about getting the price right. And in a competitive environment, that is the only number the customer really sees.

If you want to find out more about how ePAL Global can help you not only prepare for the new cross-border reality but also to get ahead of it and optimise your product catalogue as well as your fulfilment and shipping flow, feel free to visit www.ePALGlobal.eu/landing if you are a WooCommerce user or www.ePALGlobal.com if you use a different platform or custom-developed web store.

Read on for part III in the series.

[…] …this is the first post in a two (or maybe three) post series… part II is available here. […]

[…] the second [“The €3 flat rate duty (pt.II)”], we asked another simple […]